Find out why a 6-bedroom house may need tailored home insurance and what insurers usually check.

9

min read

If your home has six or more bedrooms, arranging home insurance may not always be as straightforward as it is for a smaller standard property.

This does not mean your home is uninsurable. However, some standard home insurance products are designed around limits, such as the number of bedrooms, rebuild cost, contents value or type of property. Once a home falls outside those limits, you may need a more tailored policy.

A six-bedroom house may also have a higher rebuild cost, more extensive contents, larger living areas, outbuildings, specialist features or a layout that is more complex to insure.

This guide explains why larger houses can need a different approach, what insurers may look at, and what to check before arranging cover.

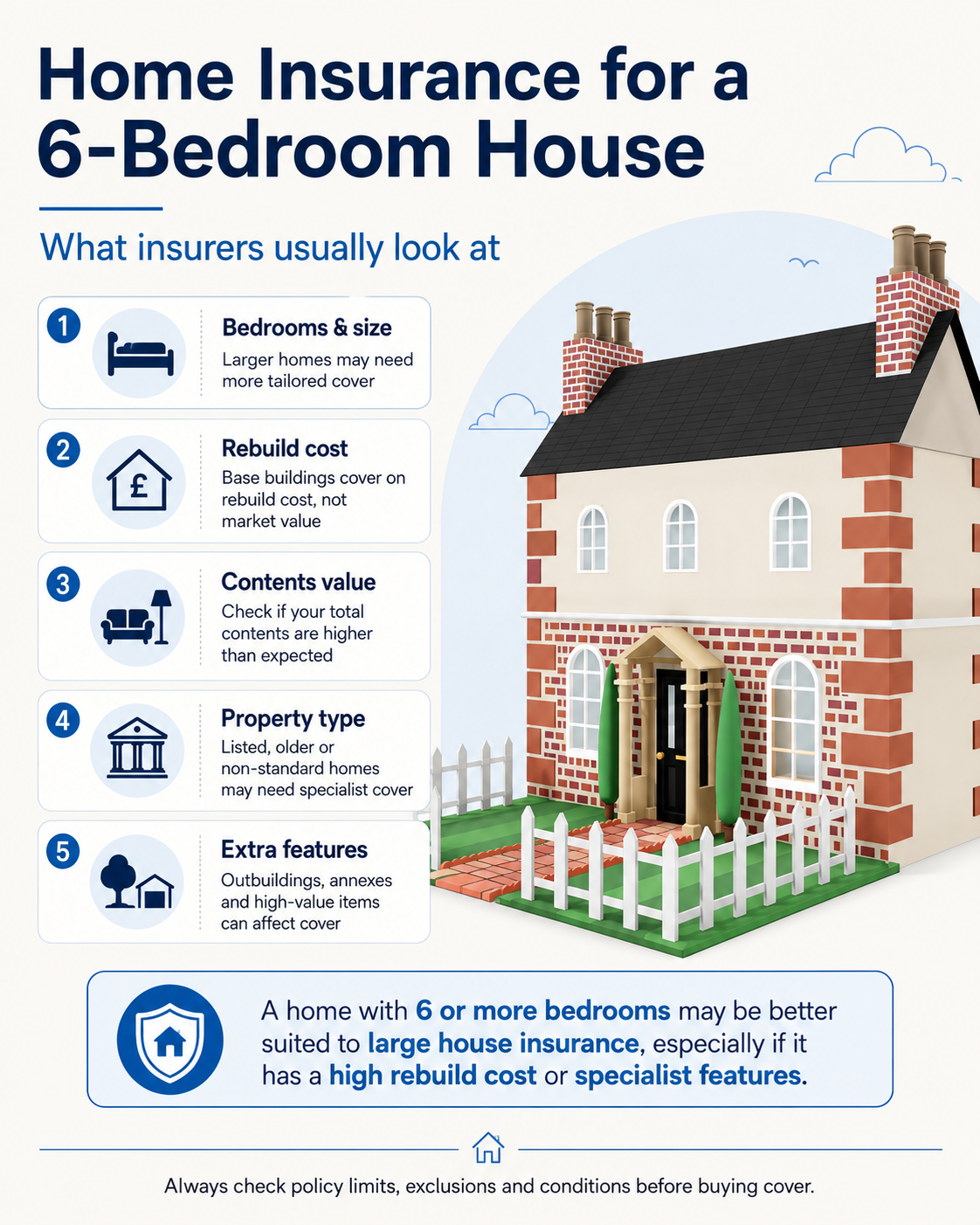

Why can a 6-bedroom house be harder to insure?

A six-bedroom house is usually larger than a typical family home. For insurers, that can affect both the likelihood and potential cost of a claim.

Larger homes may have:

higher rebuild costs

more rooms and a larger floor area

more extensive contents

higher-value furniture, jewellery, art or collections

outbuildings, garages, annexes or leisure features

older or more complex construction

more bathrooms, pipework and heating systems

higher repair costs after fire, flood, storm or escape of water

The number of bedrooms is only one factor. A modern six-bedroom home on a standard estate may be very different from a large period property, listed building, converted farmhouse or country house with outbuildings.

Because of this, insurers usually need to understand the property as a whole, not just the number of bedrooms.

Is a 6-bedroom house always classed as a large house?

For insurance purposes, a house with six or more bedrooms will often be treated as a larger home. However, there is no single rule that applies across every insurer.

Some insurers may focus on the number of bedrooms. Others may look more closely at the rebuild cost, floor area, contents value, property type, age, construction materials or claims history.

This is why it is important to answer quote questions carefully. Two homes with the same number of bedrooms may need very different levels of cover.

Why do some insurers stop at 5 bedrooms?

Some standard home insurance products are built for properties that fit within set limits. These limits may include the number of bedrooms, the rebuild value, the contents value, the occupancy type or the construction of the property.

In some cases, a home with more than five bedrooms may fall outside a standard insurer’s appetite. That does not necessarily mean the property is unusually risky. It may simply mean the insurer’s standard product was not designed for that type of home.

This is one reason why homeowners sometimes run into problems when using online quote journeys. The property may be too large for the questions or limits behind the quote system.

If this happens, it is usually better to look for cover designed for larger homes rather than trying to fit the property into a policy that may not reflect it properly.

What buildings cover might a large house need?

Buildings insurance is designed to cover the structure of your home. This can include the walls, roof, floors, fitted kitchens, bathrooms and other permanent fixtures, subject to the terms of the policy.

For larger houses, the buildings sum insured is especially important. This figure should be based on the cost of rebuilding the property, not the market value.

Your rebuild cost may include:

labour and materials

demolition and site clearance

architects’, surveyors’ and professional fees

rebuilding the property in its current form

specialist materials or features, where relevant

A home’s rebuild cost can be very different from its sale price. A property may have a high market value because of its location, but a lower rebuild cost. In other cases, especially with older, listed or unusual properties, the rebuild cost may be higher than expected.

If you are unsure, it may be worth getting a professional rebuild valuation, particularly if the home is large, listed, unusual or has not been valued for insurance purposes for several years.

Yes, cover may be available for larger homes with higher rebuild requirements.

At Intelligent Insurance, our large house insurance can provide buildings cover up to £1,000,000, with the option to increase this for specific cases. This can be helpful for larger homes where a standard buildings limit may not be enough.

The right level of cover will depend on the property itself, including its size, structure, age, materials, location and rebuild cost. You should always check the policy documents, schedule, limits, exclusions and conditions before buying cover.

What information should you check before getting a quote?

Before arranging insurance for a six-bedroom house, it helps to have the right information ready.

Useful details may include:

the number of bedrooms

the property’s rebuild cost

the approximate contents value

details of high-value items

the year the property was built

the type of construction

whether the property is listed

whether there are outbuildings, annexes or garages

any history of flooding, subsidence or previous claims

whether the property is your main home, second home or let property

whether the property is ever left unoccupied for long periods

Providing accurate information is important. If the number of bedrooms, rebuild value or property details are incorrect, this could affect the suitability of the policy or cause problems if you need to make a claim.

What about contents insurance for a large house?

Larger homes often contain more belongings, and the total contents value can be higher than expected.

Contents insurance can cover items such as furniture, clothing, electrical items, carpets, curtains and personal possessions kept in the home, subject to the terms of the policy.

When estimating contents, it is easy to understate the value. A room-by-room approach can help. Start with the larger items, then include smaller belongings such as kitchen equipment, books, clothing, bedding, tools and decorative items.

You should also check whether any items need to be specified separately. This may apply to jewellery, watches, art, antiques, musical instruments, collections, bicycles or other higher-value possessions.

What if the property is listed, old or non-standard?

Many larger homes also have features that can affect insurance.

For example, the property may be:

listed

built before 1900

timber-framed

stone-built

thatched

part flat-roofed

undergoing renovation

affected by previous subsidence

used as a second home or holiday home

These features do not automatically mean cover is unavailable. However, they can mean the property needs a more specialist approach.

A listed building may require specialist materials and repair methods. An older property may have non-standard construction or period features. A home undergoing renovation may have different risks from a fully occupied main residence.

If more than one specialist factor applies, it is usually worth speaking to an insurer or broker that deals with non-standard homes.

Underinsurance happens when the amount of cover is too low for the cost of repairing, rebuilding or replacing what is insured.

For a large house, this can be a particular concern because rebuild and contents values may be higher than expected.

To reduce the risk of underinsurance:

check that the rebuild cost is realistic

do not rely only on the market value

review the figure after major building work

update the contents value when you buy expensive items

specify high-value items where required

check single-item limits

review your policy at renewal

ask for professional advice if the property is unusual or high value

The aim is not just to get a policy in place. It is to make sure the policy reflects the home properly.

Key points to remember

A six-bedroom house can usually be insured, but it may not always fit standard home insurance products.

The number of bedrooms is important, but insurers may also look at rebuild cost, contents value, construction, property age, occupancy, claims history and specialist features.

If your home has six or more bedrooms, a high rebuild value or more complex insurance needs, a tailored large house insurance policy may be more suitable than a standard policy.

At Intelligent Insurance, we provide home insurance for large houses, high-value homes and properties with higher rebuild or contents requirements. Our large house insurance can include buildings cover up to £1,000,000, with the option to increase for specific cases.

Yes, many six-bedroom houses can be insured, but they may need a more tailored policy. Some standard home insurance products have limits around bedroom numbers, rebuild cost or contents value.

Why do insurers ask how many bedrooms my house has?

The number of bedrooms helps insurers understand the size and potential value of the property. It may also affect the rebuild cost, contents value and potential claim size.

Is a house with more than 5 bedrooms harder to insure?

It can be. Some standard insurers may not cover homes with more than five bedrooms, while others may need more information before offering a quote.

How much buildings cover do I need for a large house?

Your buildings cover should be based on the cost of rebuilding your home, not its market value. For larger, older or unusual homes, a professional rebuild valuation may be useful.

Can contents insurance be included for a 6-bedroom house?

Yes, buildings and contents cover can often be arranged together. Larger homes may have higher contents values, so it is important to estimate your belongings carefully and check policy limits.