Rebuild Cost Guide: Why It Matters for Your Home Insurance

This guide explains what rebuild cost means, why it is important, and when you may need specialist advice.

8

min read

When arranging buildings insurance, one of the most important figures you may be asked for is your home’s rebuild cost.

This is not the same as the market value of your property. It is the estimated cost of rebuilding your home from scratch if it were destroyed beyond repair.

Getting this figure right matters. If your rebuild value is too low, your home may be underinsured. This could mean there is not enough cover to meet the full cost of repair or rebuilding after a serious claim. In some circumstances, your insurer may also reduce the amount paid, depending on the terms of your policy.

Rebuild costs have also changed significantly in recent years. The cost of materials, labour, professional fees and other building-related expenses has risen, meaning a figure that seemed suitable several years ago may no longer reflect the true cost of rebuilding today.

This guide explains what rebuild cost means, why it is important, and when you may need specialist advice.

What is rebuild cost?

Your home’s rebuild cost is the estimated amount it would cost to completely rebuild the property if it were destroyed.

This can include:

labour and building materials

demolition and site clearance

architects’, surveyors’ and other professional fees

the cost of rebuilding the property in its current form

specialist materials or features, where relevant

For buildings insurance, the rebuild cost helps determine the amount of cover needed for the structure of your home.

It is important to remember that this is only about rebuilding the property. It is not the same as what your home would sell for on the open market.

Rebuild cost vs market value

A home’s market value is the amount it might sell for. It can be affected by location, land value, local demand, transport links, schools and many other factors.

A home’s rebuild cost is different. It focuses on the cost of reinstating the building itself.

For many standard properties, the rebuild cost may be lower than the market value. However, this is not always the case. Some homes may cost more to rebuild than their sale price, especially if they include specialist materials, period features or unusual construction methods.

For example, a listed building, timber-framed home or stone-built property may need specialist labour and materials. These can increase the cost of rebuilding.

Rebuild costs are not fixed. They can rise over time as the cost of labour, materials and professional services changes.

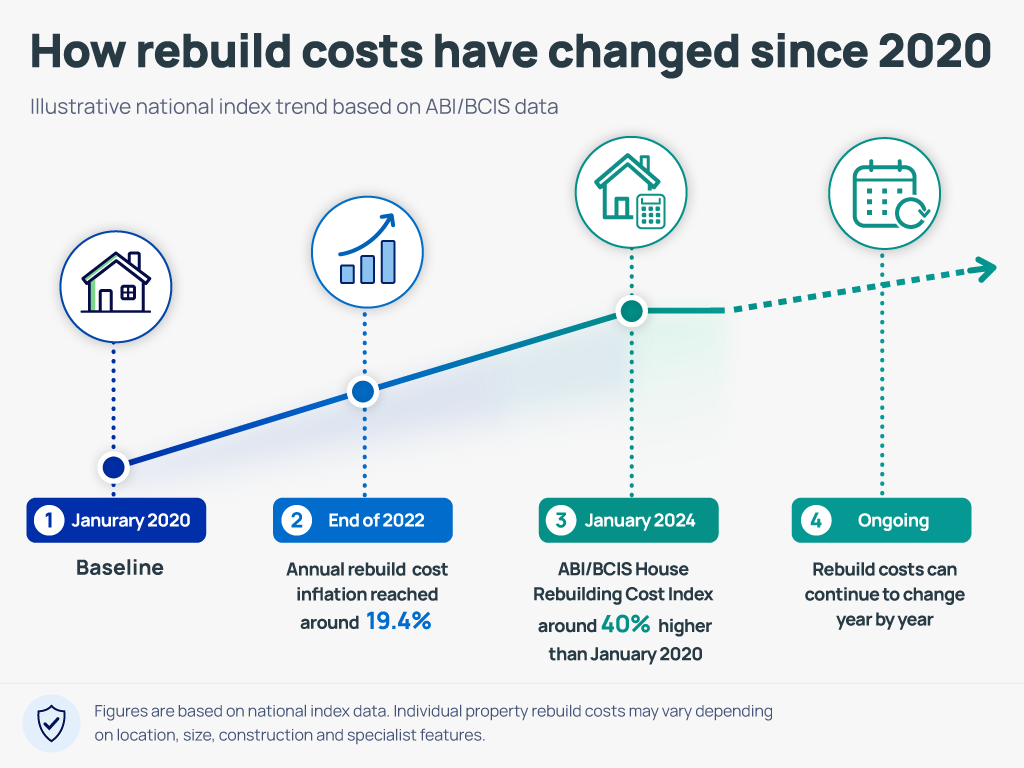

In recent years, rebuild costs have increased sharply. According to BCIS, annual growth in the ABI/BCIS House Rebuilding Cost Index was 19.4% at the end of 2022. BCIS later reported that the index was 40% higher in January 2024 than it was in January 2020.

That does not mean every property’s rebuild cost has increased by exactly the same amount. Individual homes can vary depending on size, construction, location, materials, access and specialist features.

However, it does show why it is important not to rely on an old rebuild estimate for too long.

Why underinsurance can be a problem

Underinsurance can happen when the amount of cover is not enough to meet the full cost of rebuilding or repairing your home.

For example, if your home would cost £400,000 to rebuild, but your buildings insurance is based on a rebuild value of £250,000, there may be a significant shortfall.

This can create problems if you need to make a claim. Depending on the policy wording and the circumstances, your insurer may reduce the amount paid. Some policies include an “average clause”, which can reduce a claim in proportion to the level of underinsurance.

This is why it is important to provide a rebuild value that is as accurate as possible, based on the information available to you.

The aim is not to overestimate or underestimate, but to make sure your buildings cover reflects the likely cost of rebuilding your home.

In these cases, the cost of rebuilding may be affected by specialist labour, planning requirements, conservation rules, bespoke materials or the need to rebuild using traditional methods.

If your home is non-standard, listed or has special architectural features, it may be sensible to speak to a chartered surveyor for a more accurate rebuild assessment.

How can you check your rebuild cost?

There are several ways to check or estimate your rebuild cost.

Use a rebuild cost calculator

For many standard homes, a rebuild cost calculator can provide a useful starting point. These tools usually ask for details such as the property type, age, construction, number of floors, floor area and postcode.

However, calculators are usually based on standard assumptions. If your home is unusual, listed, made from non-standard materials or has specialist features, the result may not be accurate enough on its own.

Check your survey or mortgage valuation

If you bought your home recently, your mortgage valuation, homebuyer report or building survey may include a rebuild figure.

This can be useful, but it may still need reviewing if the report is several years old, if rebuild costs have changed, or if you have altered the property since then.

Ask a chartered surveyor

A professional rebuild valuation from a chartered surveyor may be more suitable if your home is complex, listed, high value, non-standard or difficult to assess.

Although there is usually a cost for this, it can provide a more reliable figure than a general online estimate.

Review after major changes

You should also review your rebuild value if you have made changes to your home, such as:

building an extension

converting a loft or garage

adding outbuildings

carrying out major renovations

changing the structure or layout

adding high-value fixtures or specialist features

These changes may affect the cost of rebuilding the property.

Do you need to give a rebuild estimate for buildings insurance?

In many cases, you may be asked to provide or confirm a rebuild value when arranging buildings insurance.

Some policies may offer a set buildings cover limit, while others may ask for a specific rebuild estimate. Even where a cover limit is provided, it is still important to make sure it is enough for your property.

Your insurer or broker may be able to explain what information is needed. However, the declared rebuild value should be based on the best information available to you.

If you are unsure, especially if your home is non-standard, you may wish to seek professional advice.

For more detail, see our FAQ: Do I need to give a rebuild estimate to get buildings insurance?

When should you review your rebuild value?

It is a good idea to review your rebuild value regularly, especially at renewal.

You should also check it if:

you have not reviewed it for several years

your property has been extended or renovated

you have added outbuildings or specialist features

your home is listed or non-standard

you are relying on an old survey or valuation

rebuild costs have changed significantly

your policy documents show a figure you are unsure about

Reviewing your rebuild value does not have to mean starting from scratch every year. But it is worth checking whether the figure still feels suitable, especially if there have been changes to your home or wider building costs.

Key points to remember

Your rebuild cost is the estimated cost of rebuilding your home, not its market value.

If your rebuild value is too low, your home may be underinsured. This could affect the amount available if you need to make a claim.

Rebuild costs have risen significantly in recent years, so old estimates may no longer be suitable.

Online calculators can help with standard homes, but they may not be accurate for listed, unusual or non-standard properties.

If your home has specialist features, unusual construction or complex rebuilding needs, a chartered surveyor may be the best way to obtain a more reliable rebuild figure.

The rebuild value you declare should be based on the best information available to you. Checking it regularly can help make sure your buildings insurance remains suitable for your home.

Need help arranging insurance for a non-standard home?

At Intelligent Insurance, we help customers arrange home insurance for a wide range of properties, including listed buildings, period homes, unoccupied properties, homes undergoing renovation and properties made from non-standard materials.

What is the difference between rebuild cost and market value?

Market value is what your home might sell for. Rebuild cost is the estimated cost of rebuilding the property if it were destroyed. The two figures can be very different.

Can my rebuild cost be higher than my market value?

Yes. This can happen if your home has specialist materials, listed status, period features or unusual construction. In some cases, the cost of rebuilding may be higher than the property’s sale value.

Is an online rebuild calculator always accurate?

No. A calculator can be useful for many standard homes, but it may not be suitable for listed buildings, non-standard construction, unusual materials or architecturally complex homes.

Who is responsible for checking the rebuild value?

Your insurer or broker may provide guidance, but the rebuild value you declare should be based on the best information available to you. If you are unsure, you may wish to seek advice from a chartered surveyor.

What happens if my rebuild value is too low?

If your rebuild value is too low, your home may be underinsured. This could mean there is not enough cover to meet the full cost of repair or rebuilding. In some circumstances, your insurer may reduce the claim payment, depending on the policy terms.

This guide explains why unoccupied home insurance claims are sometimes declined, the most common underlying reasons, and you can reduce the risk of issues if you need to claim.