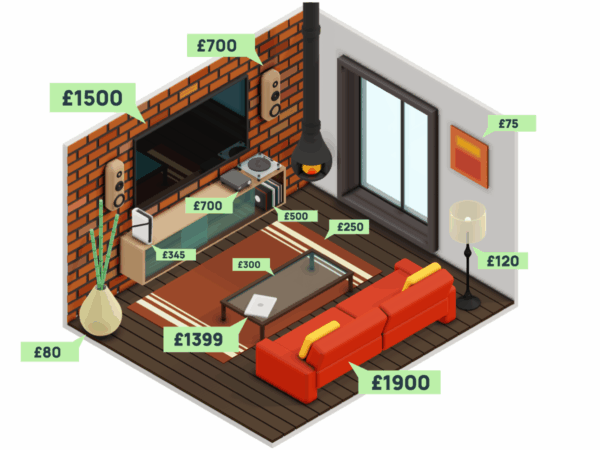

Find out how to Value Your Home Contents for Insurance

This guide explains how to work out the total value of your possessions & why accurate valuation is important.

5

min read